Open Banking may have started as a bank‑led initiative, but the ecosystem has expanded into a much more diverse and collaborative landscape. Traditional banks remain crucial, particularly in safeguarding sensitive financial data and ensuring compliance with regulatory standards. Evolving frameworks – such as PSD2/PSD3 in Europe and emerging Open Banking rules in other regions – are strengthening requirements for both banks and fintech providers, helping to maintain consistent levels of security and consumer protection.

At the same time, customers are increasingly turning to fintech‑first solutions – such as neobanks, digital wallets and payment apps – as important financial touchpoints. Many of these services connect to bank data via standardised Open Banking APIs, reducing reliance on older methods like screen scraping, which is being phased out in favour of regulated, API‑based access in many markets.

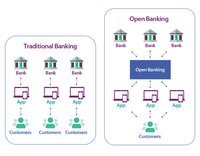

For financial institutions, Open Banking APIs provide a powerful way to modernise legacy systems and collaborate with fintech and non‑bank platforms. Through embedded finance, banking capabilities can be surfaced directly inside e‑commerce, mobility and other digital experiences, rather than only through a bank’s own channels. As a result, the traditional distinction between “banking app” and “partner app” is blurring, with customers increasingly accessing financial services wherever they are needed.

Looking ahead, Open Banking is increasingly seen as part of a wider move toward Open Finance and Open Data. Open Finance extends secure data sharing to areas such as investments, pensions, savings and insurance, while Open Data explores interoperability beyond banking into other sectors. Alongside this, banks and fintechs are starting to apply analytics and, in some cases, AI‑based models on top of Open Banking data to provide real‑time insights, personalised recommendations and more proactive financial guidance for customers.